Weekly Corn Market Update 06/23/23

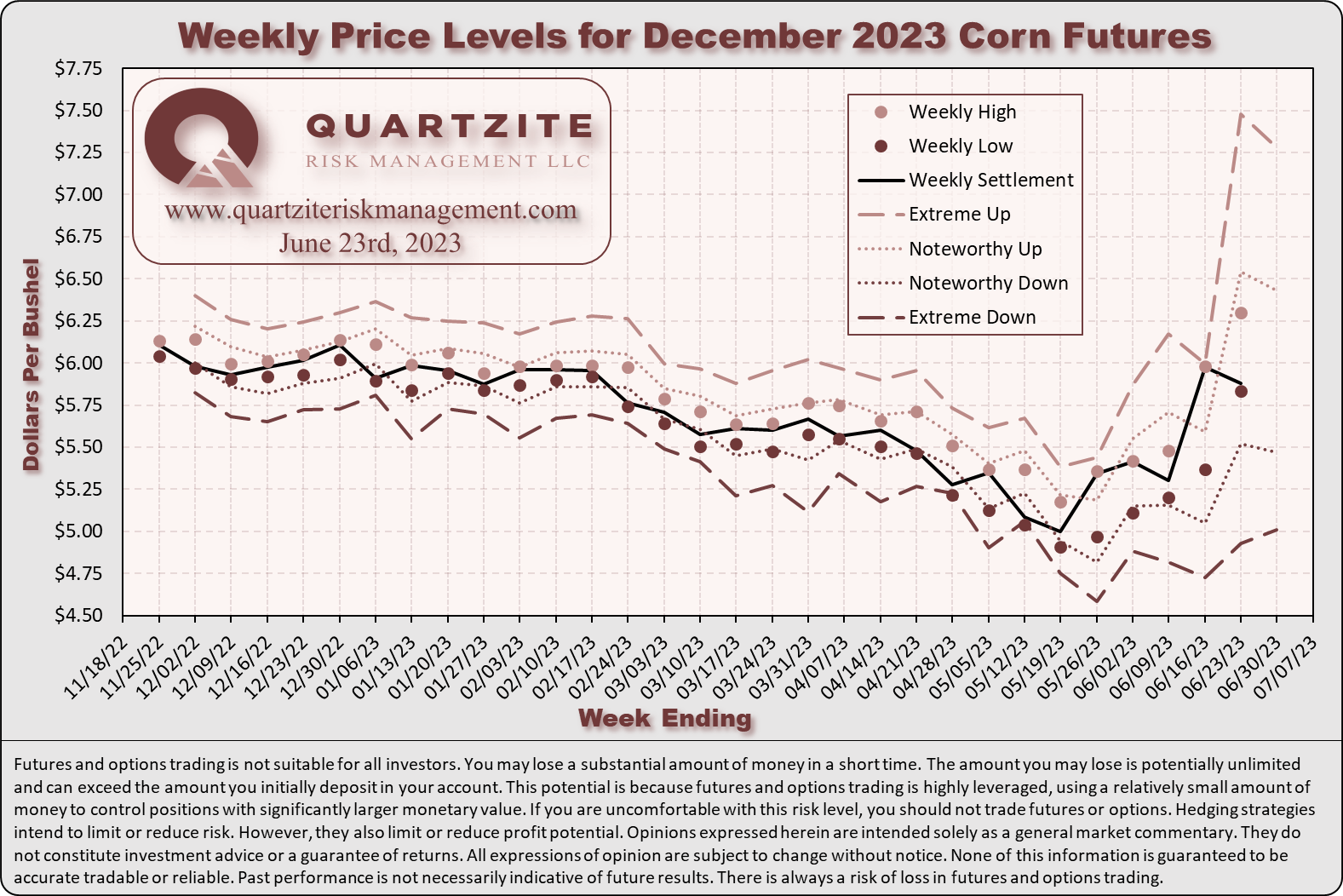

December 2023 (Dec23) corn futures (the benchmark for 2023 corn production) finished the week lower by 9.50 cents (~1.59%), settling at $5.8800/bushel. This week's trading occurred within the unremarkable band we published last week.

Our corn demand index (CDI) outperformed Dec23 corn futures this week - falling only 1.02%. The ratio of Nov23 soybean futures divided by Dec23 corn futures decreased from 2.25 to 2.23. Potential instability in the US financial system, the war in Ukraine, executive branch policy, increasing tensions with China, Federal Reserve interest rate policy, and the Dollar remain concerns. The USDA releases its Quarterly Grain Stocks and Annual Acreage reports on Friday.

Dec23 corn futures are still above the long-term downtrend trendline extending from the highs of 04/27/22 and 10/14/22 - currently in the neighborhood of $5.75/bushel. We see technical levels below the market at around $5.84, $5.71, $5.63, $5.48, $5.25, $5.14, $4.98, $4.83, $4.63, and $4.20/bushel. We see technical levels above the market at around $6.03, $6.14, $6.31, $6.55, and $6.78/bushel. The $5.84 level seems particularly important considering that the 200-day moving average is in the same vicinity, and the area has been critical in the past. Given that, we think the market is at a reasonable place to wait out this weekend's updated weather forecasts and possibly next Friday's USDA release. Most daily and weekly momentum indicators finished the week in neutral territory, though some daily indicators remain in overbought territory. Carry spreads from Dec23 to Mar24, May24, and Jul24 widened this week.

Our at-the-money model volatilities for the 2023 crop finished the week lower. Excepting short-dated Aug23, our new crop model volatilities are lower than comparable volatilities a year ago. Our primary focus remains trading around our clients' established positions to capture market volatility to help offset time decay. See the model volatility charts below for more details. One compares our closing at-the-money model volatilities for this week and last. The other compares our current model volatilities with the forward volatilities they imply between consecutive expirations.

For next week's trading in Dec23 corn futures, we consider trade in the $5.4700-$6.4300 per bushel range unremarkable. Notable moves extend to the $5.0100-$7.200 per bushel range. Price action beyond that would be extreme. Here is a short note on these levels for those that have not read the Guide to Understanding our Weekly Corn Market Update: We derive these levels from listed option prices and the volatilities we use in our model to approximate them. If they still seem wide for next week, they are. The demand for options remained quite elevated this week, reflecting continued uncertainty in the options market. Be sure to visit our Twitter page to vote in our weekly poll. While you are there, please give us a follow.

For the fall crop insurance price, we see a median of $5.6750/bushel with a mode between $5.35 and $5.40/bushel. The fall crop insurance price distribution shifted slightly lower with the selloff. Similar to our weekly price levels, we derive this distribution from listed options prices. When the demand for options is high, you can expect a correspondingly wide distribution. See the crop insurance charts below.

This week, we made several trades for our Quartzite Precision Marketing customers in the 2023 corn crop. On Tuesday morning, with short-dated Jul23 implied volatility down considerably from last Friday's close, we purchased a near-the-money straddle. Later, on Tuesday, we paid less than a penny for the out-of-the-money short-dated Jul23 puts we sold last Thursday, booking a small winner. On Wednesday, we bought some near-the-money short-dated Jul23 puts to hedge some of the deltas resulting from the gamma in the straddle we purchased the day before. On Friday, as the market approached the strike of the straddle we purchased Tuesday, we bought Dec23 futures against the short-dated Jul23 puts we purchased on Wednesday, effectively leaving us with just Tuesday's straddle. Near the close on Friday, we liquidated the short-dated Jul23 straddle from Tuesday for the small amount of meat left on the bone. All told, our trading in short-dated Jul23 had only a small net effect on PnL at the end of the week, but it allowed us to weather this week's volatility comfortably while leaving us room if the market continued its march in either direction. In addition to these trades for the 2023 crop year, we dipped a toe into 2024. For several clients with enough diesel usage to justify it, we traded a futures spread by purchasing Apr24 heating oil futures (generally considered a good proxy for diesel fuel) and selling Dec24 corn futures on a ratio.

#AgTwitter & #oatt - cast your vote in this week's poll, then click over to read our Weekly #Corn #Market Update: https://t.co/ZofsiyOJaV

— Quartzite Risk Management LLC (@QuartziteRMLLC) June 24, 2023

We think these scenarios have roughly equal probability next week. Where do you think #cbot Dec23 corn #futures will settle next week?

If you think Quartzite Precision Marketing might be a good fit for your operation, reach out to learn more and discuss your options.

Thanks for taking the time to read. We look forward to your questions and feedback. Thanks again.

(970)223-5297 - Email - Contact Form - Twitter - Facebook

Weekly Price Levels and Corn Demand Index

As a reminder, the Quartzite Risk Management Corn Demand Index references the weekly change in April 2024 futures for Crude Oil, Live Cattle and Lean Hogs. We weigh the percentage change in those contracts and compute the index's percentage change. Crude Oil accounts for 50% of the index, and Live Cattle and Lean Hogs each make up 25%. To create the chart, we started the index at the Dec23 corn futures settlement on 11/04/22; then added or subtracted the index's weekly percentage change. We want to add a few warnings. First, there are only a handful of data points - not much to go on. Second, the index references relatively illiquid markets - making any strategy based on it challenging to execute. Third, we expect divergences to increase as we get into the growing season when the corn market will likely look more toward supply for its direction. In short, we would not attempt to trade on this information without much more data, nor would we recommend anyone else does.