Weekly Corn Market Update 04/23/21

Author's note: I want to apologize for the late release this week. I have been traveling and could not get time to write until Sunday morning.

Thanks for your patience,

James

December 2021 (Dec21) corn futures (the benchmark for 2021 corn production) finished the week higher by 38.50-cents (~7.52%), settling at $5.5075/bushel. This week's price action took place in a 45.00-cent (~8.78%) true range measured from last week's settlement. The week's high was 10.00-cents above the upper-extreme range we published last week, and the weekly settlement was 3.50-cents above that level.

This week, our corn demand index (CDI) rose ~0.75%, underperforming Dec21 corn futures again and continuing to signal that the corn market may be overheating relative to demand. See the chart below. Concerns over COVID-19 in the U.S. are mostly gone as widespread vaccination continues. Still, some potential problems remain with the possibility of new strains and other parts of the world enacting renewed shutdowns in response to resurgent outbreaks. Uncertain executive branch policy, interest rates, and their impact on the Dollar remain significant concerns. We believe these factors will continue to provide potential sources of volatility for the foreseeable future. Russian and Ukrainian tensions appeared to ease this week, with Russia reducing its forces at the Ukrainian border.

The uptrend that started from the August 2020 lows remains intact this week, with Dec21 trading at fresh intraday highs on Thursday in addition to posting new daily and weekly high settlements. Various daily and weekly momentum indicators display highly overbought conditions. Carry spreads from Dec21 to Mar22, May22, and Jul22 narrowed again this week. Given the parabolic nature of the rally over the last few weeks, we would not be surprised by a sharp reversal.

Implied volatilities for the 2021 crop exploded higher this week. Reasonable values for long-term hedgers are extremely challenging to find at these levels. The forward volatility implied between Dec21 and Mar22 strengthened considerably this week - making Mar22 less attractive than in past weeks. However, May22 volatility was soft relative to other expirations and has become our preferred expiration - see the forward volatility chart below. Opportunistic spreading and careful position management are still virtual necessities to maintain the flexibility needed to manage production uncertainty and volatility risk. See the charts below. One compares our closing at-the-money model volatilities for this week and last. The other compares our current model volatilities with the forward volatilities they imply between consecutive expirations.

Looking ahead to next week's trading in Dec21 corn futures, we would consider movement within the $5.2925-$5.7500 per bushel range to be unremarkable. Notable moves would extend to the $4.9850-$6.1900 per bushel range. Price action beyond that would be extreme. You will find a chart comparing these levels to the corresponding weekly price action below. Be sure to visit our Twitter page to vote in the poll we hold there each week. While you are there, please give us a follow.

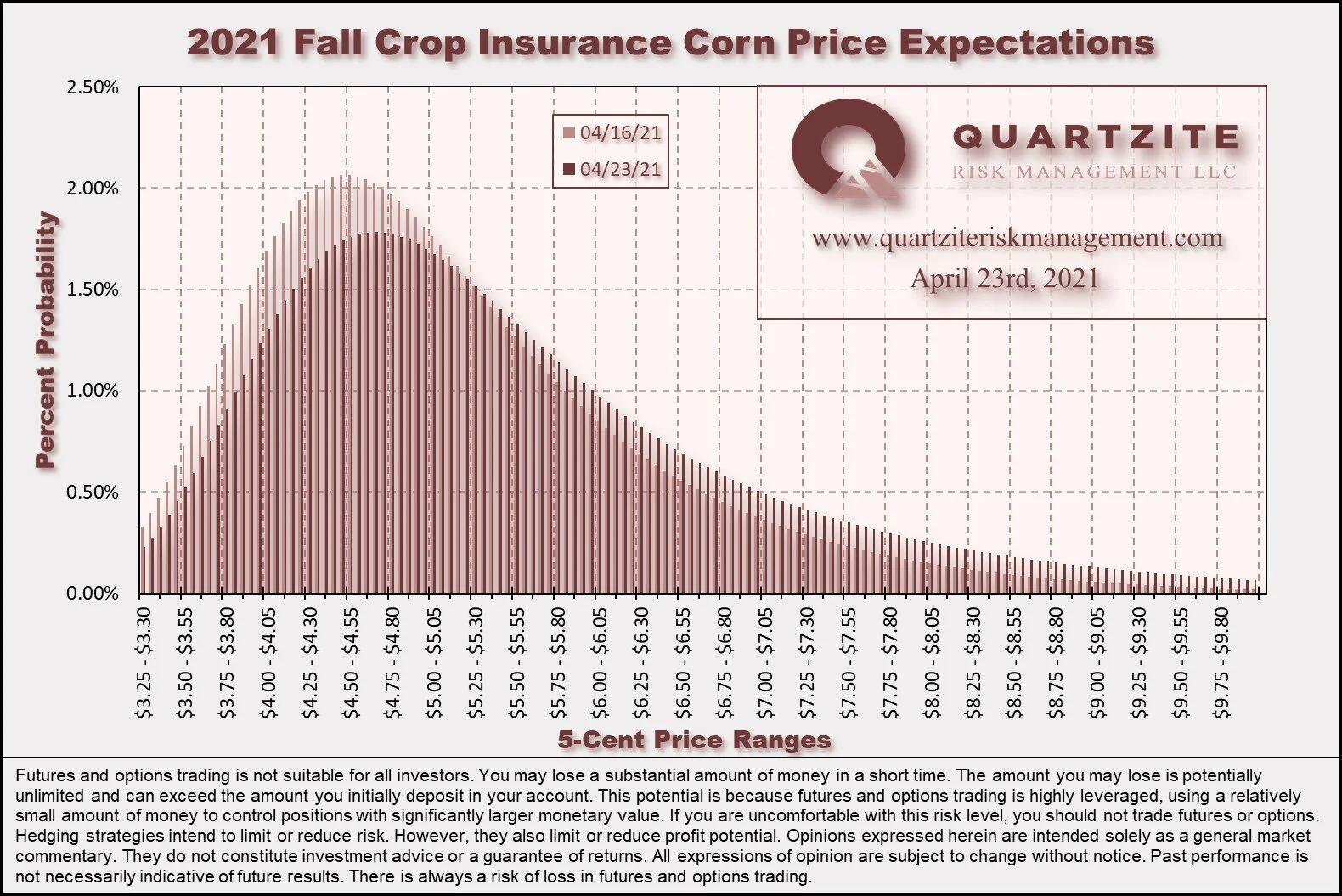

Our Crop Insurance Fall Price distribution shifted much higher this week due to the rally. It also widened considerably due to increased implied volatility. See below for distribution and cumulative probability charts for fall crop insurance prices and a chart highlighting the distribution's changes.

We made several trades in the corn complex for our Quartzite Precision Marketing customers this week. We made sales (futures and synthetic futures) on Tuesday and Thursday against expiring May in-the-money calls we purchased two weeks ago in front of the April WASDE. After Thursday's rally, we made several trades to reposition our clients' overall portfolios. These trades generally got them less long the market or moved options closer to at-the-money and included various options spreads, cash contracting, and futures sales. We used the compression in carry spreads this week to shorten the duration of our hedges by buying longer-dated futures contracts and replacing them with nearer-term sales. On Friday, May22 downside puts traded low relative to other expirations, and we added a significant position in them. Overall, we remain somewhat long the market. This length continues to be more out of necessity than desire. Still, it dissipates quickly to the downside as our options kick in.

Thanks for taking the time to read. We look forward to your questions and feedback. Please feel free to contact us via our contact form, Facebook, Twitter, email, or phone at (970)294-1379. Thanks again. Have a great week.

#AgTwitter & #oatt Another week, another new high. Cast your vote in this week's poll, then click over to read our Weekly #Corn #Market Update:https://t.co/ZgpuP7V3o3

— Quartzite Risk Management LLC (@QuartziteRMLLC) April 25, 2021

We think these scenarios are equally likely for next week. What do you think?

Will Dec21 corn #futures settle?

Weekly Price Levels and Corn Demand Index

As a reminder, the Quartzite Risk Management Corn Demand Index references the weekly change in April 2022 futures for Crude Oil, Live Cattle and Lean Hogs. We weigh the percentage change in those contracts and compute the index's percentage change. Crude Oil accounts for 50% of the index, and Live Cattle and Lean Hogs each make up 25%. To create the chart, we started the index at the Dec21 corn futures settlement on 11/20/20; then added or subtracted the index's weekly percentage change. We want to add a few warnings. First, there are only a handful of data points - not much to go on. Second, the index references relatively illiquid markets - making any strategy based on it challenging to execute. Third, we expect divergences to increase as we get into the growing season when the corn market will likely look more toward supply for its direction. In short, we would not attempt to trade on this information without much more data, nor would we recommend anyone else does.